Outright Purchase vs 0% Instalment Plan: Cash Flow vs Control for Solar in Malaysia

Last updated: 7 Nov 2025

Explore how paying upfront or through a 0% Instalment Plan affects your cash flow, control, and long-term savings when installing solar.

So, you’ve decided to install solar panels – great choice! But now comes a big decision: should you pay for your system outright or choose a 0% credit card instalment plan (IPP)?

Both options give you ownership of your solar system from day one, but they work very differently when it comes to cash flow, flexibility, and long-term savings.

This article breaks down the pros, cons, and real-life numbers so you can choose the option that matches your financial comfort zone.

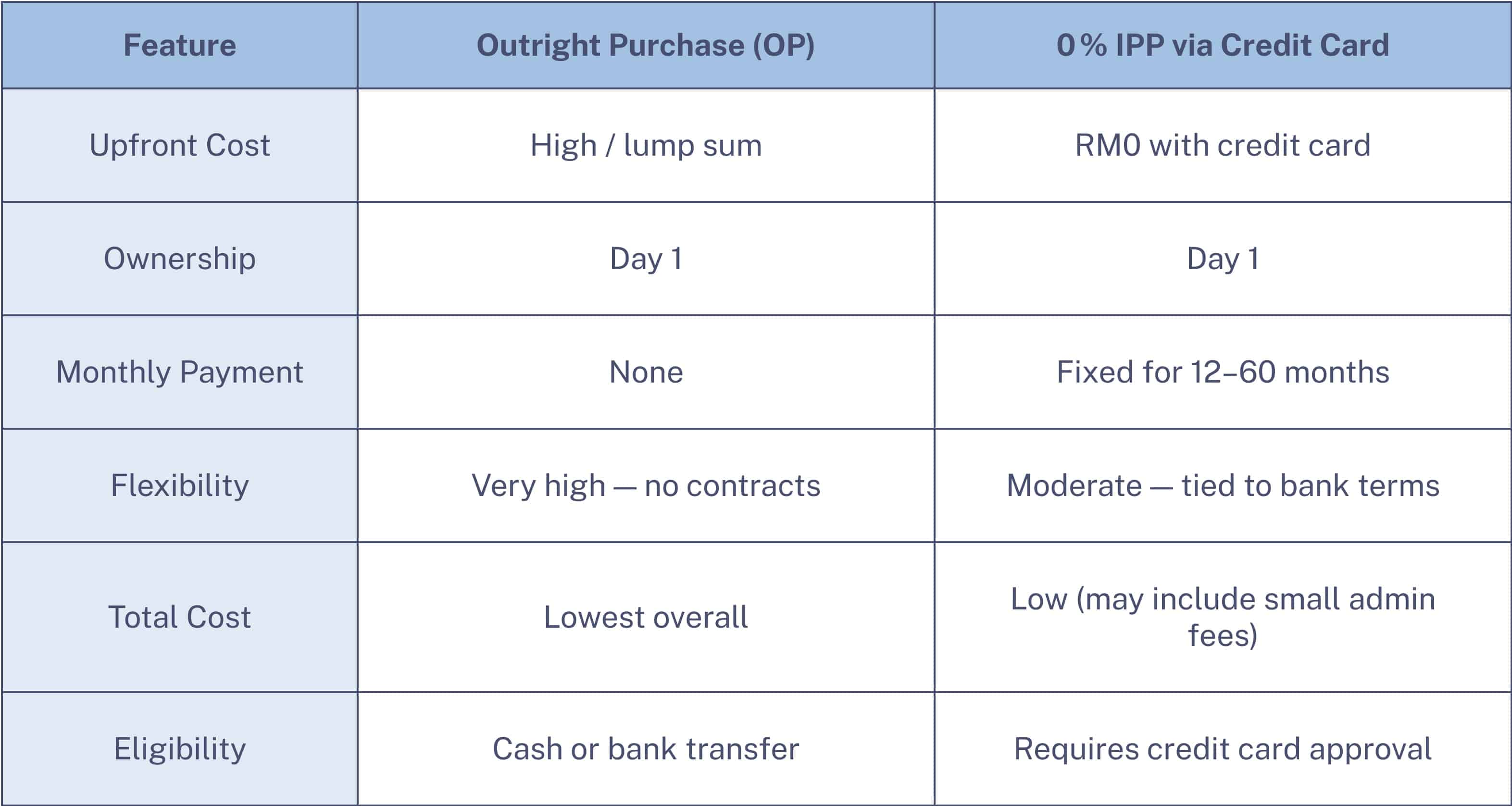

What Is Outright Purchase (OP)?

Outright Purchase means paying for your solar system in full.

- Upfront Cost: Full payment upfront (RM25,000–RM45,000 for most homes).

- Ownership: Immediate. You own the system from day one.

- Flexibility: High – no contracts, no interest, no repayment obligations.

- Extras: Warranty and free first-year maintenance are included.

What Is a 0% Instalment Plan (IPP)?

A 0% Instalment Plan allows you to split payments using your credit card.

- Upfront Cost: RM0 upfront with eligible banks.

- Payment Term: Spread payments over 12–60 months (1–5 years).

- Ownership: Immediate – the system is yours once installed.

- Eligibility: Requires a participating credit card.

- Extras: Warranty and free first-year maintenance included.

Let's Compare

Who Should Choose Outright Purchase?

- Homeowners with available savings who want the lowest total cost.

- Families planning to stay in their home long-term and maximise ROI.

- Buyers who value full control and no repayment obligations.

Who Should Choose 0% Instalment Plan (IPP)?

- Families who prefer to spread payments without paying interest.

- Homeowners who want immediate ownership but can’t afford full upfront cost.

- Buyers who already have a credit card and want easy, predictable payments.

Real-Life Example

Let's say you're installing a 8 kW system worth RM 30,000

Outright Purchase:

RM30,000 upfront, ROI in ~4-5 years.

0% IPP (60 months):

RM500/month for 5 years. ROI in 5 years.

Both options give you ownership immediately, but the difference is how you manage your cash flow.

Conclusions

Choosing between Outright Purchase and 0% Instalment Plan comes down to cash flow vs control:

- Outright Purchase is the best if you want the lowest cost overall and have the capital ready.

- IPP is ideal if you want to keep your cash flow flexible while still owning your system immediately.

Either way, solar pays off in the long run. Want to explore which plan works best for your home? Contact us today!